Capital Gains – BIG Hole in Your Trust?

Categories: Estate Planning, Time to Update Trust, Trust and Estate Attorney

Let’s begin with a simple Q & A…

Let’s begin with a simple Q & A…

QUESTION: How could the terms of my trust increase capital gains tax?

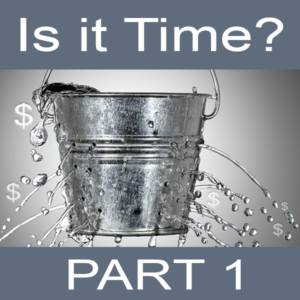

ANSWER: If you have a trust drafted prior to 2012, you may have an old trust that was drafted to minimize estate tax at the expense of increasing capital gains tax. If you fail to update the trust it’s as though there’s a MASSIVE HOLE in the bucket. Yikes! You really need to plug the leak so the money doesn’t drain away! This article, and others in this series, will shed helpful light on what you need to know on the topic.

If you have questions and don’t feel like reading, you’re welcome to call the office at 408-364-1234 and make an appointment. Newcomers receive a FREE 30-minute Legal Consultation. At our appointment I can look over the trust and tell you what it says. Or, if I drafted it, simply call. I will look at my file and let you know if there is potential hole or something to consider. There may be a straight-forward fix. Now, on with the article!

Do You Know What Your Trust Says?

Really! Try reading it. If your trust was drafted prior to 2012 it may contain language that would stump a Rhodes Scholar; never mind a regular person. There was a very good reason for that type of drafting prior to the new estate tax laws that began with the 2000 tax act.

Time for a story that you’ll want to read! Names and details have been changed to protect privacy and help make a point. Bear with me…

A new client, “Mrs. Smith,” came in to see me the other day. She and her husband set up their living trust in 1982 with another attorney. At that time the estate tax laws were vastly different from what they are today.

Keep in mind that back in those days the best way to avoid or minimize estate taxes was to have the trust divide, after the death of the first spouse, into two to three separate shares (OK – sometimes even more!). This minimized or eliminated the estate tax, which started at a tax rate of 55% for every dollar over $600,000.

With this kind of planning, a couple could shelter up to $1,200,000 from estate tax, instead of the $600,000, resulting in a savings to the children of about $192,800. Woo hoo! The downside, however, was freezing the income tax basis* of appreciated assets in an irrevocable trust. In general, it was considered a fair trade in a fairly stable market, with a combined state and federal capital gains tax at 25%.

*income tax basis is usually the original purchase price plus any improvements the owner puts into the property while owning it. Any capital gains on sale by the owner are computed by subtracting the owner’s income tax basis from the sale price. Example: I buy 10 shares of stock for $100.00. $100.00 is my income tax basis. I hold the stock for two years, and then sell the stock for $120. The capital gain is $20 ($120-$100).

Back to Mrs. Smith

They set up their trust in 1982 with another attorney, and her husband died in 1989. At that time the couple had $1,000,000 in assets. Following the terms of the trust, Mrs. Smith worked with her prior attorney to allocate the trust assets between the Survivor’s Trust and the Credit Shelter Trust ($500,000 each). Among the assets was a rental condominium in Sunnyvale, and at the time of Mr. Smith’s death the condominium was valued at $200,000 and allocated to the Credit Shelter Trust as part of the $500,000.

Mrs. Smith is coming to see me simply because she wants to change the trustee, and NOT because she was aware of a particular problem. Mrs. Smith is about to be very happy, and this is why… that condominium in Sunnyvale is now worth $1,400,000. Great news! Right?

Well, wait a minute. When Mrs. Smith dies, the condominium will distribute to her children with an income tax basis of $200,000. They will sell it for $1,400,000 (or higher), and have a capital gain of $1,200,000. The capital gains tax is approximately $300,000 ($1,200,000 x .25).

Fortunately, there is a solution. Even though the Credit Shelter Trust is irrevocable, we can use the Court to modify the trust, and solve this problem. If Mrs. Smith and her children agree, we can ask the Court for an order modifying the trust, and save the children $300,000 in taxes!

AND… we can solve this problem even if both spouses are deceased, so long as we catch it before assets are distributed out of the trust.

Have Questions About Updating Your Trust?

It’s important to take a fresh look at your trust to see if there are any BIG HOLES in the bucket. There is more on this topic if it’s 2am and you are reading this in your jammies… Click to read about Mr. Jones in Part 2 of this series!

Better yet, make an appointment with me for the FREE 30-minute Legal Consultation, during which I will look over the trust and tell you what it says. If I was the one who drafted it, call me. I’ll take a look at my file, and let you know if there is something of interest that you may want to discuss further.

Either way, let’s find and plug any leaks so that money stays in your bucket where it belongs!

Diane M. Brown, Esq.

Diane M. Brown, Esq.

Working every day to keep my clients out of court!

It’s your money… Let’s keep it that way!

Call 408-364-1234

This blog contains general information and is not meant to apply to a specific situation. Please seek advice of counsel before proceeding as each case is unique.

No comments yet.